What is meant by company valuation?

A company valuation is a process in which the economic value of a company is determined. The entire company or only parts of the company (business units) can be valued. For example, a company must be valued if it is to be sold or merged with another company. The valuation is also important for tax reporting. Valuations are often carried out by professional consultants.

There are many different methods for valuing companies. A company valuation can include an analysis of the company management, the capital structure, the future earnings prospects or the market value of the assets. The tools used for valuation can vary depending on the company and industry. Common approaches to business valuation include auditing financial statements, discounting cash flow models and also comparisons of similar companies.

Methods of company valuation

Valuing a company is a very complex process but not an exact science. There are many methods for valuing a company. Some of them are presented below:

Market capitalization

The use of market capitalization is one of the simplest methods. Market capitalization is calculated by multiplying the share price by the number of shares in circulation. For example, the market capitalization of Bell Ltd is CHF 1.76 billion. The number of shares in millions is 6.28 and the share price is around CHF 280 (as at 21.02.2022). Market capitalization is therefore the valuation of a company on the stock exchange.

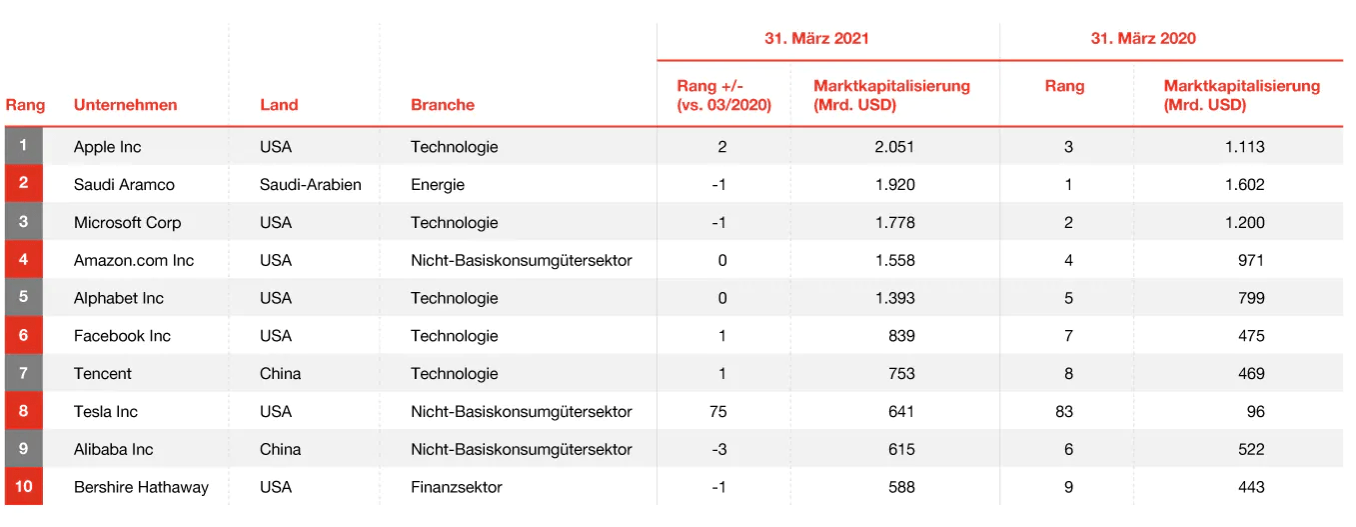

The company with the highest current market capitalization (as at 21.02.2022) is Apple, followed by Saudi Aramco and Microsoft.

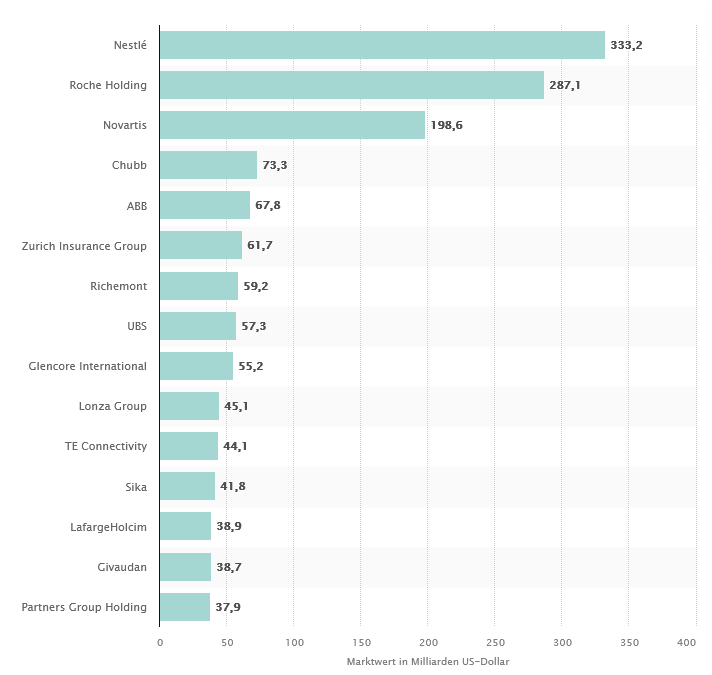

The largest Swiss company is Nestlé with a market value of USD 333.2 billion, followed by Roche and Novartis.

List of the 10 most valuable companies by market capitalization

Source: www.pwc.de

The 15 largest Swiss companies by market value on April 16, 2021

Quelle: www.statista.com

Market value methods – the use of multipliers

So-called multiples can be used to value listed companies. For example, the prices paid on the stock exchange (trading multiples) can be used here. Multiples can be, for example, sales, EBITDA, EBIT, net profit, price/earnings ratio or the price/book ratio.

In the company valuation method using the turnover factor (temporal turnover method), a turnover stream generated over a certain period of time is given a multiplier that depends on the industry and the economic environment. For example, a technology company can be valued at three times turnover, while a service company can be valued at 0.5 times turnover.

Enterprise value = turnover x turnover multiplier

Instead of the sales multiple, the profit multiple can also be used to get a more accurate picture of a company’s true value, as a company’s profits are a more reliable indicator of its financial success than sales. Different profit ratios can be used for profit, as the following examples of sales multiples show:

Enterprise value = EBITDA x EBITDA multiplier

Enterprise value = EBIT x EBIT multiplier

Enterprise value = Net profit x Net profit multiplier

where:

EBITDA = earnings before interest, taxes, depreciation and amortization

EBIT= earnings before interest and taxes

Discounted cash flow method

The discounted cash flow method is used to determine the fair value of a company based on future cash flows. The series of cash flows that an investor expects over the duration T of the investment is added to the terminal value. The free cash flow serves as the base value. The free cash flow is the cash flow that could be distributed without affecting the current business plans. The cash flows are discounted using a tax-adjusted weighted average cost of capital(WACC). See also Discounted cash flow (DCF) for the formula and specific examples.

EVA method

Economic Value Added (EVA) is a measure of a company’s financial performance. EVA can also be referred to as economic profit, as it attempts to capture the actual economic profit of a company. EVA is the difference between the rate of return (RoR) and the cost of capital of a company. If a company’s EVA is negative, this means that the company is not creating any value with the funds invested in the company.

EVA = NOPAT – (invested capital x WACC)

where:

NOPAT: Net operating profit after taxes

Invested capital: Borrowed capital + finance leases + equity

WACC: Weighted average cost of capital

The aim of EVA is to quantify the cost of investing capital in a business and then assess whether it generates enough cash to be considered a good investment. A positive EVA shows that a project is generating returns in excess of the minimum required rate of return.

In an EVA-based company valuation, the present value of the future EVA is determined first. If the capital invested at the beginning of the period under review and the terminal value are added to the present value of the future EVA, the result is the enterprise value. In theory, the DCF and EVA methods should lead to the same result.

Book value

This is the value of a company’s equity as shown in the balance sheet. The book value is calculated by deducting a company’s total liabilities (current and non-current liabilities) from its total assets.

Liquidation value

The liquidation value is the net present value that a company would receive if its assets were liquidated and its liabilities repaid today.

Many more methods

This is by no means an exhaustive list of the business valuation methods in use today. Other methods include replacement value, break-up value, asset-based valuation and many more.